Cart Before the Horse: Michael Burry’s AI Reality Check

In nine words, Michael Burry has done what he does best: thrown cold water on a narrative that has captivated markets, Silicon Valley, and the financial press. While Elon Musk enthusiastically shared a viral illustration depicting artificial intelligence’s inevitable ascent past human intelligence, Burry’s response cuts to the heart of what may be the defining investment mania of the 2020s.

The timing is characteristically Burry. As AI stocks have driven market valuations to historic levels, as companies race to rebrand themselves with “AI” suffixes, and as trillions of dollars flow into everything remotely connected to artificial intelligence, the man who spotted the housing bubble before anyone else is suggesting we’re putting the cart before the horse.

Decoding the Cryptic

Burry’s tweets often read like financial haikus—compressed, enigmatic, requiring interpretation. “Cart before monkey robot people” is vintage Burry, but the message becomes clear when parsed:

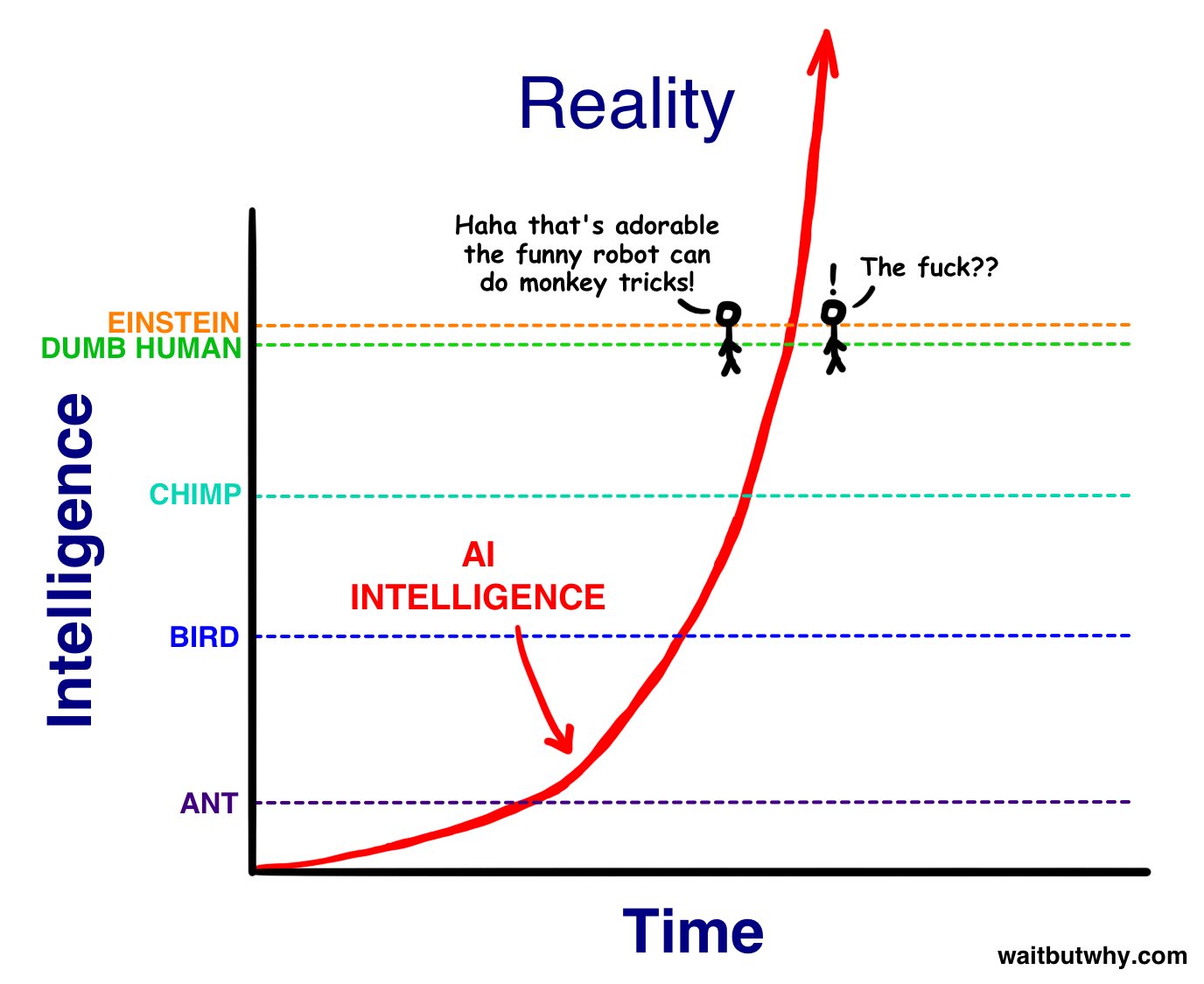

“Cart before the horse” is the obvious idiom—we’re getting ahead of ourselves. But Burry characteristically adds layers. “Monkey robot people” is likely a reference to the viral chart itself, which shows a stick figure marveling at AI doing “monkey tricks” before the intelligence explosion occurs. The implication: we’re still at the party trick stage, celebrating parlor games while pricing in the singularity.

“No one has invented AI yet” is the declarative kicker. This isn’t Burry denying that impressive machine learning systems exist. It’s Burry making a precise distinction that the market has entirely collapsed: what we’re calling “AI” today is not artificial intelligence in any meaningful sense.

The Intelligence That Isn’t

The chart Musk endorsed illustrates a common narrative in Silicon Valley: AI will follow an exponential curve, starting below human intelligence, then rapidly surpassing it, rocketing past Einstein-level cognition into realms we can’t comprehend. This is the “intelligence explosion” theory, the technological singularity, the stuff of both utopian dreams and dystopian nightmares.

Burry’s point is more fundamental: we’re not on that curve yet. We haven’t invented the thing that’s supposed to explode. What we’ve created are sophisticated pattern-matching systems, statistical models that can generate text and images by training on massive datasets. These are powerful tools—transformative even—but they are not intelligent in the way the chart suggests.

Current AI systems don’t understand anything. They don’t reason from first principles. They don’t form intentions, question assumptions, or grasp causality in the way even a child does. GPT-4, Midjourney, Claude—these are impressive statistical engines, but calling them “artificial intelligence” is like calling a mechanical calculator “artificial mathematics.” The name inflates the achievement while obscuring what’s actually been accomplished.

The Trillion-Dollar Presumption

This distinction wouldn’t matter much if it were merely semantic. But the market has valued companies and entire sectors based on the presumption that we’re already on the exponential curve depicted in that chart. Nvidia’s market cap exceeds the GDP of most nations based largely on being the pickaxe seller in what’s assumed to be an intelligence gold rush. Microsoft, Google, Amazon—their valuations embed expectations of AI-driven productivity revolutions.

- Global AI investment: $200+ billion annually

- Nvidia market cap growth: ~$2 trillion (2023-2026)

- AI-related ETFs: 300% average growth since 2023

- Venture capital AI deals: 40% of all tech funding

- Companies adding “AI” to their name: Stock price average increase of 30%

But what if Burry’s right? What if “no one has invented AI yet” in the sense that matters for these valuations? What if we’re in a period analogous to the 1990s internet bubble, where the technology was real and transformative, but the valuations were pricing in a future that arrived much later and differently than expected?

The Dot-Com Parallel

Burry has seen this movie before. In the late 1990s, the market didn’t question whether the internet would be transformative—it obviously was. The error was in assuming transformation would be immediate, universal, and most importantly, that it would accrue primarily to the first-movers being valued at astronomical multiples.

Pets.com had internet. Webvan had internet. Boo.com had internet. They all went to zero. Amazon had internet too—and spent years being mocked for its lack of profitability before eventually dominating. The technology was real; the timeline, business models, and value capture were wildly mispriced.

Today’s AI landscape echoes this pattern. We have genuine technological advancement—transformative pattern-matching capabilities that will certainly change how we work and create. But we’re pricing in artificial general intelligence, autonomous reasoning, and an intelligence explosion that hasn’t been invented yet.

Monkey Tricks vs. Understanding

The “monkey tricks” phrase is particularly cutting because it captures how we’re evaluating current AI capabilities. A large language model that can write code or generate images feels magical—the same way a calculator felt magical to someone who previously did arithmetic by hand. But we don’t confuse calculators with mathematicians.

Current AI systems excel at:

- Pattern completion based on training data

- Statistical prediction of likely next tokens

- Interpolation within known domains

- Mimicking styles and formats they’ve seen

Current AI systems struggle with or cannot do:

- Novel reasoning outside their training distribution

- Understanding causality vs. correlation

- Genuine abstraction and conceptual thinking

- Recognizing when they don’t know something

- Forming intentions or goals independent of prompts

These aren’t minor gaps—they’re the difference between a tool and an intelligence. And if Burry’s right that “no one has invented AI yet” in the meaningful sense, then the gap between current capabilities and what’s priced into markets is a chasm.

The Counter-Narrative

To be fair, Burry’s skeptics have a case. Every revolutionary technology looked impossible until it wasn’t. Experts said heavier-than-air flight was physically impossible in 1900; the Wright Brothers flew in 1903. Nuclear reactions were theoretical curiosities until they suddenly weren’t. The progression from GPT-2 to GPT-4 was faster and more significant than most predicted.

Maybe we’re closer to artificial general intelligence than Burry thinks. Maybe the exponential curve is steeper than historical precedent suggests. Maybe “monkey tricks” are actually a more advanced stage than they appear, and we’re months rather than decades from the inflection point where AI systems begin to meaningfully understand rather than pattern-match.

But this is precisely where Burry’s track record becomes relevant. He has a history of being early to structural problems that consensus dismisses. And in markets, being early looks identical to being wrong until the correction arrives.

The Valuation Problem

Even if we grant that artificial general intelligence is coming—even if we accept the exponential curve is real and we’re early on it—there’s still the valuation question. How much is it worth today that AGI might arrive in 5 or 10 or 20 years?

The current market pricing suggests it’s worth trillions. But consider what’s embedded in these valuations:

- That AGI will be achieved

- That it will be achieved soon

- That it will be achieved by the companies currently leading

- That these companies will be able to capture and monetize the value

- That governments won’t regulate away the profits

- That the technology won’t be quickly commoditized

Every one of these assumptions needs to be true for current valuations to make sense. Burry’s “cart before the horse” critique suggests we’re assigning high probability to a chain of contingent events, each of which is highly uncertain.

The “No One” Caveat

Burry’s phrase “no one has invented AI yet” deserves careful parsing. He doesn’t say “AI will never be invented” or “AI is impossible.” He says no one has done it yet. This is the same Burry who correctly identified housing bubble dynamics years before they mattered—not because he predicted houses would never appreciate, but because he recognized unsustainable fundamentals.

The implication isn’t that AI advancement is fake or that current systems are worthless. It’s that there’s a categorical difference between impressive machine learning systems and artificial general intelligence, and the market is pricing as if that difference has already been bridged.

Historical Precedent

History offers multiple examples of genuine technological revolutions that nonetheless destroyed early investor capital:

- Railways (1840s): Transformative technology, massive speculation, Railway Mania bubble, most investors wiped out

- Automobiles (1920s): Obviously revolutionary, hundreds of car companies funded, 99% went bankrupt

- Radio (1920s): RCA peaked at $114/share in 1929, fell to $2.50 by 1932, despite radio transforming communication

- Internet (1990s): Correctly identified as revolutionary, Nasdaq fell 78% from peak, most dot-coms failed

In each case, the technology was real and transformative. In each case, early investors were mostly destroyed. The pattern isn’t that revolutions don’t happen—it’s that markets consistently overpay for early-stage revolutionary technologies, creating bubbles that burst even as the underlying technology succeeds.

What Burry Might Be Seeing

Based on his track record and investment philosophy, Burry likely sees several red flags in current AI mania:

Narrative-driven rather than fundamentals-driven pricing. Companies’ valuations are moving based on AI announcements and associations rather than demonstrated profitability improvements. This is classic bubble behavior—price follows story rather than cash flows.

Confusion between potential and achievement. The market is pricing in endpoints (AGI, full automation, productivity revolution) while we’re still at starting points (advanced autocomplete, pattern matching). The gap between current capability and priced-in future is reminiscent of dot-com era projections.

First-mover assumption fallacy. History suggests technological revolutions typically benefit later entrants who learn from early mistakes, not first movers who spend capital figuring out what doesn’t work. Yet current leaders are priced as if they’ve already won a race that hasn’t really begun.

Ignoring the infrastructure-to-application timeline. Even if AGI arrives tomorrow, the timeline from “invention exists” to “invention generates profits that justify current valuations” is typically measured in decades, not quarters. The market rarely prices this lag correctly.

The Singularity Skepticism

The chart Musk endorsed depicts the standard singularity narrative: slow progress, then explosive superintelligence. But this narrative itself is worth questioning. What if intelligence doesn’t work that way? What if the curve isn’t exponential but logarithmic—each increment of advancement requiring exponentially more resources?

We’re already seeing hints of this. The progression from GPT-3 to GPT-4 required massive increases in compute, data, and funding. Early reports suggest GPT-5 requires even more dramatic resource scaling. If intelligence advancement requires exponential increases in resources for linear improvements in capability, we’re not on the explosive curve the chart depicts—we’re on a resource-constrained crawl.

Burry’s skepticism might reflect recognition of these scaling challenges. “No one has invented AI yet” could be shorthand for: “The path from here to AGI is far harder and longer than markets assume.”

The Contrarian Play

Burry doesn’t typically share his investment positions publicly, but his tweet suggests potential positioning. If he believes AI valuations are disconnected from reality—if the “cart is before the horse”—the contrarian play would be shorting AI-inflated stocks or sectors.

This would be classic Burry: identifying a consensus narrative built on shaky foundations, finding instruments to profit from an eventual repricing, and enduring mockery from consensus bulls until vindication arrives. It worked with dot-com stocks. It worked spectacularly with mortgage-backed securities. Could it work with AI-hyped equities?

The challenge, as always with Burry, is timing. Being right about fundamentals but wrong about timing can be financially catastrophic. AI stocks could continue inflating for months or years before reality asserts itself. The market can remain irrational longer than you can remain solvent.

What This Means for Investors

If Burry’s perspective has merit, what should rational investors do? The answer isn’t necessarily to short everything AI-related. The answer is to make crucial distinctions:

Distinguish between AI beneficiaries and AI bubbles. Companies that use AI tools to improve margins and productivity are different from companies valued entirely on AI narrative. Microsoft using AI to improve Office is different from a startup worth billions because it has “AI” in its pitch deck.

Question exponential assumptions. When a valuation implies AI will automate 40% of white-collar work in 3 years, ask whether current capabilities support that timeline. When projections show hockey-stick revenue growth from AI products, ask what assumptions underpin those projections.

Remember that transformative ≠ profitable. The internet transformed everything. Most internet companies went bankrupt. AI will likely transform everything too. That doesn’t mean most AI companies will be profitable, or that current valuations reflect realistic profit potential.

Consider the deployment lag. Even truly revolutionary technologies take time to deploy, integrate, and generate returns. The gap between “invention exists” and “invention drives corporate profits sufficient to justify market cap” is usually measured in decades.

The Bigger Picture

Burry’s tweet, characteristically terse, points to something deeper than one man’s skepticism about one technology trend. It highlights a recurring pattern in financial markets: the tendency to price in the destination before the journey has begun.

The chart Musk endorsed shows AI intelligence rocketing past human capability into superintelligent realms. Maybe that happens. Maybe it happens soon. But Burry’s pointing out that we’re pricing as if it’s already happened, or as if the path from current large language models to artificial general intelligence is a straight line rather than an uncertain journey through technical, commercial, and regulatory obstacles.

“Cart before monkey robot people” translates to: You’re celebrating and pricing in the destination while you’re still watching trained parrots perform tricks. Impressive tricks, certainly. Revolutionary parrots, perhaps. But parrots nonetheless.

Conclusion

Michael Burry’s nine-word response to AI euphoria won’t stop the momentum. Bulls will continue pointing to impressive demos, breakthrough capabilities, and exponential curves. Companies will keep adding “AI” to their investor presentations. Markets will likely continue rewarding anything AI-adjacent.

But Burry has a history of being right about structural problems that consensus misses. When he suggests we’re putting the cart before the horse—that we’re pricing in artificial intelligence before anyone has actually invented it—investors would be wise to at least consider the possibility.

The question isn’t whether AI will be transformative. It will be. The question is whether current valuations reflect realistic assessments of what’s been achieved versus what’s been assumed, and whether the timeline from impressive demos to profit-generating deployment is being honestly evaluated. If Burry’s right that “no one has invented AI yet” in the sense that matters for current valuations, we’re in for a painful repricing.

As always with Burry, the timing remains uncertain. But the analytical framework—distinguishing between genuine achievement and narrative-driven speculation—is worth considering. Especially when the monkey tricks are receiving standing ovations and trillion-dollar valuations.

The Mathematics of Looking Like an Idiot: Burry on Value Investing

The Mathematics of Looking Like an Idiot: Burry on Value Investing

The Hidden Cost of AI’s Gold Rush: Burry on SBC and the ROIC Illusion

The Hidden Cost of AI’s Gold Rush: Burry on SBC and the ROIC Illusion

The Commoditization of Compute: Burry’s Warning on Infrastructure Spending

The Commoditization of Compute: Burry’s Warning on Infrastructure Spending

From Market Crashes to Nuclear Reactors

From Market Crashes to Nuclear Reactors

Michael Burry vs WSJ: Why Being Early Isn’t Being Wrong

Michael Burry vs WSJ: Why Being Early Isn’t Being Wrong

The AI Reckoning: Michael Burry’s Warning on the Next Great Write-Off

The AI Reckoning: Michael Burry’s Warning on the Next Great Write-Off

Too Big to Save: Michael Burry on the AI Bubble and the Illusion of Rescue

Too Big to Save: Michael Burry on the AI Bubble and the Illusion of Rescue